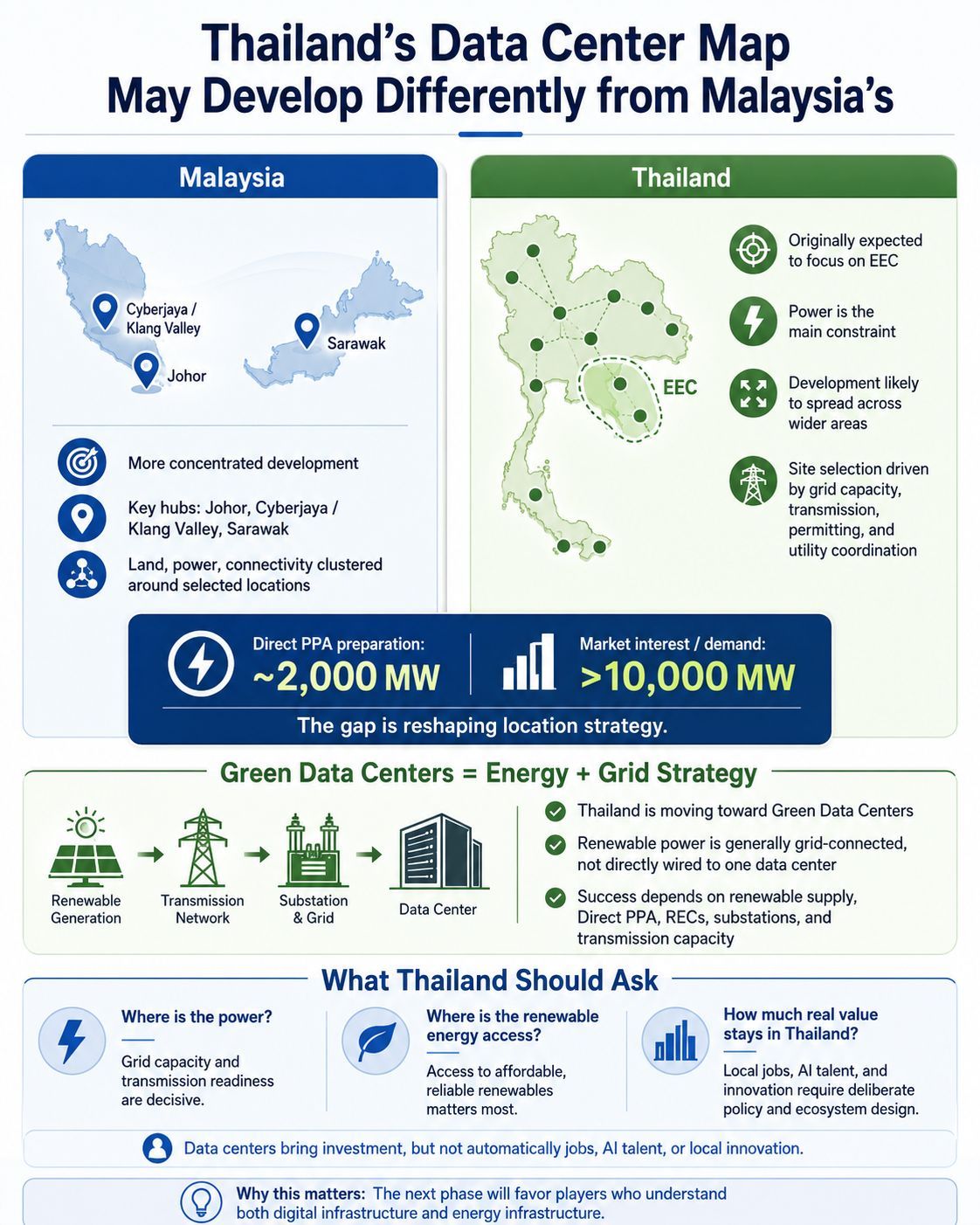

In Thailand, power is the real constraint and the biggest factor in site selection, not just land, says Sam Lu, Senior Business Development Manager, Italthai Engineering, in a recent Linkedin post.

”Grid capacity, transmission availability, permitting, land readiness, and utility coordination will become the real factors shaping the market,” he wrote.

Consequently, Thailand’s data center development may become more distributed, spreading across wider areas where power infrastructure can realistically support the demand. This means Thailand’s data center map may diverge from Malaysia’s DC development pattern, Lu opined.

Malaysia’s data center growth is becoming concentrated around key hubs such as Johor, Cyberjaya / Klang Valley, and Sarawak, where land, power, connectivity, and supporting infrastructure are clustered.

“Additionally, Thailand’s first phase of Direct PPA preparation for data centers was reportedly planned around 2,000MW. However, market interest has now exceeded 10,000MW, hence one concentrated zone, for example, the Eastern Economic Corridor (EEC) might not be able to support data center growth,” Lu revealed.

Also, with the trend towards more Green Data Centers, the proximity of projects to power infrastructure is becoming even more critical. Green DCs are powered by renewable energy which in Thailand are generally grid-connected. Power from solar farms and other renewable sources is typically sold into the grid under PPA agreements, and is not directly connected to any one specific data center.

Green Data Center development depends on a broader system: grid-connected renewable energy, Direct PPA mechanisms, renewable energy certificates, transmission capacity, substations, generation assets and clear utility coordination.

In this sense, Lu believed grid strategy is becoming data center strategy while green power strategy may become the next major deciding factor for site selection.

Perfect timing for Gulf Development

On Thailand’s richest man, Sarath Ratanavadi’s reported US$4.3 billion data center investment plan to add 2,000 megawatts of data center capacity over the next five years, Lu said it’s a natural extension of his firm, Gulf Development’s long-term position in Thailand’s energy sector.

Gulf Development Pcl is Thailand’s largest power producer.

“This is where data centers and energy infrastructure begin to overlap as data centers need reliable power, “ Lu told w.media in an interview recently.

“Gulf is not starting with land and then looking for power. Gulf is starting from power, and then building the data center opportunity around it.

“Gulf’s core strength has always been power, and data centers are fundamentally power-driven infrastructure. From that perspective, this investment appears to be a natural extension of Gulf’s long-term position in Thailand’s energy sector,” Lu said.

Gulf already has a very large conventional power base in Thailand, including six gas-fired IPP projects and 19 gas-fired SPP projects. In recent years, the company has announced 27 renewable energy projects with a combined contracted capacity of 939 MW, including 15 solar / Solar+BESS projects and 12 industrial waste-to-energy projects.

On top of that, according to the Bangkok-based executive, Gulf has secured a very significant share of Thailand’s available renewable PPA pipeline, particularly in solar and Solar+BESS giving it a major strategic advantage.

These all blend in perfectly with Gulf’s advantage and the timing couldn’t be better, said Lu.