Introduction

Recent announcements from global cloud providers and other major companies show that organisations are starting to pay close attention to reducing their greenhouse gas [GHG] emissions, and they are adjusting their mission, and purpose statements accordingly.

For the data centre sector, this has meant major revision of focus. Time spent on energy efficiency is now spent considering the carbon footprint resulting from data centre build, fit out, operation and decommission.

Scope 3 contributes greatly to this carbon footprint, and we invite you to learn from Schneider Electric on how to address Scope 3 emissions that occur throughout a data centre’s life, and how focussed data collection and analysis are the key to managing this.

What is Scope 3?

Scope 3 is usually described in the context of Scope 1 and Scope 2. These, respectively, are the direct emissions which result from the data centre operations and its GHG emission output resulting from consumption of electricity from non-renewable energy sources.

Source: “Scope 3 is the next frontier of decarbonisation in the data centre industry” presented by Mark Deguara

Source: “Scope 3 is the next frontier of decarbonisation in the data centre industry” presented by Mark Deguara

The bundling together of the three types of emissions may work against the proper understanding and management of Scope 3. Scope 1 and 2 build on the industry’s existing focus on energy. Some sources refer to Scope 3 as “everything else” – all the emissions for which the data centre is indirectly responsible (upstream and downstream along its value chain). This can include the emissions from the manufacturing and transportation of equipment for the data centre and the provision of services and materials used in construction and refit. Since Scope 3 runs through the data centre’s entire life, it is also present in waste, and at the decommissioning stages.

Why is measuring and managing Scope 3 important?

First and foremost, your brand’s reputation. It’s no coincidence that the most brand-conscious players in the data centre industry – global cloud providers – have made the boldest statements regarding their Scope 3 goals.

They have made significant progress towards reducing and/or eliminating Scope 1 and 2 sources which leaves Scope 3 as the corporate battleground. As Mark Deguara, General Manager, Data Centres at Schneider Electric, describes it:

“If you look at the Internet giants, for example, they’re now purchasing and investing in renewable energy. They’re doing everything in their power to remove that Scope 2, and they’re now trying to deal with what is included under Scope 3. If you start to look at what’s left over for them, and for data centres in general, it sits in that Scope 3 bucket significantly”.

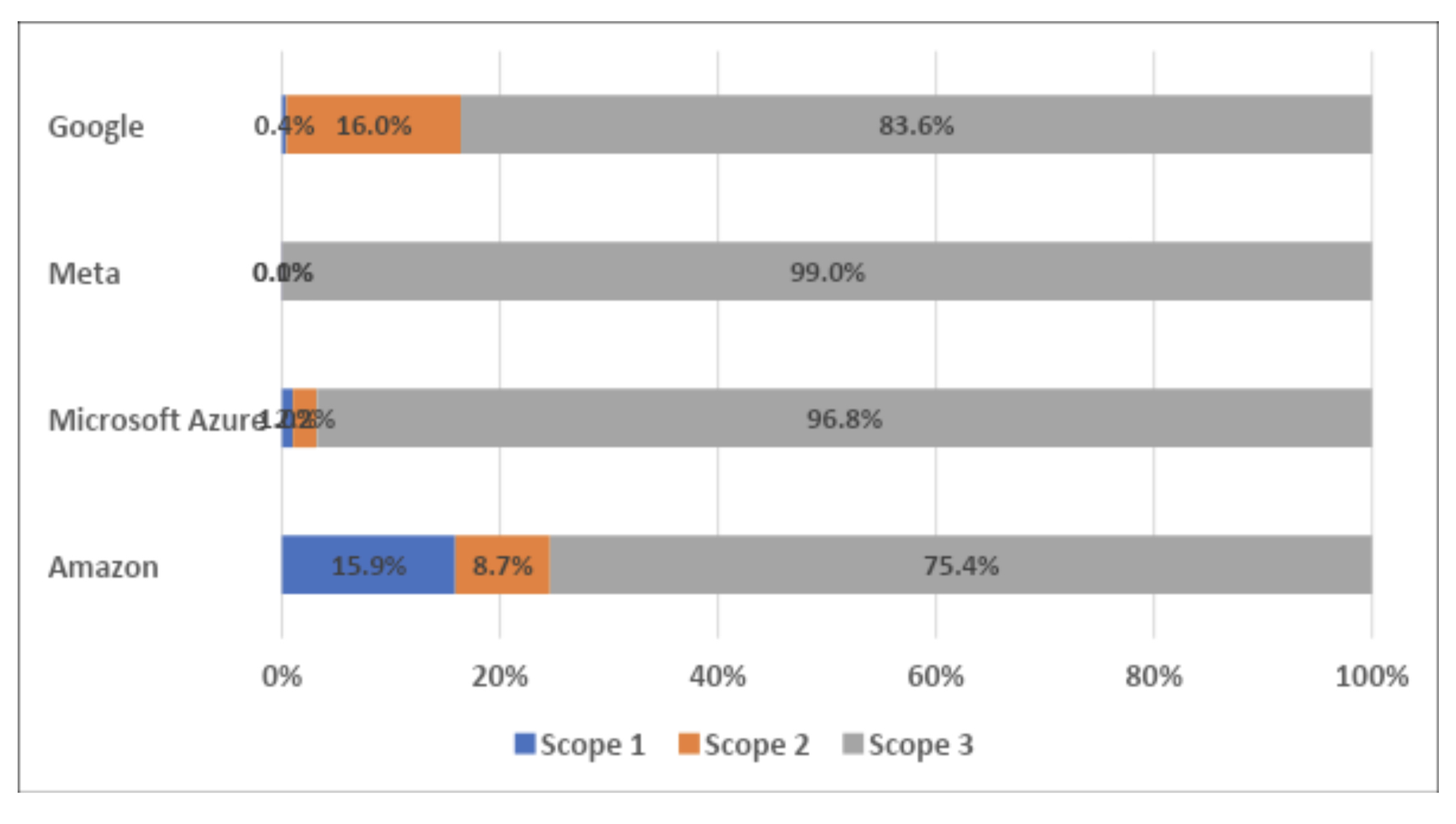

The example of the major cloud players indicates that a high majority of their carbon emissions now derive from Scope 3: 75.4% for Amazon Web Services 96.8% for Microsoft Azure; 83.6% for Google and 99% for Meta.

Sources: Schneider Electric 2023 derived from the sustainability reporting of listed organisations

Sources: Schneider Electric 2023 derived from the sustainability reporting of listed organisations

The impact on reputation can be linked directly to customer demand. As sustainability increasingly becomes a factor in enterprise decision-making, the focus of their demand has widened to take in Scope 3. This is particularly in focus as their own corporate requirements have taken it into account across their commercial activities and social responsibility.

Where technology goes, legislation will follow. In March 2022, The US Security & Exchange Commission proposed that publicly traded companies must disclose their greenhouse gas emissions and other climate-related risks to their business as part of mandatory reporting.

This reporting is due to start in 2024. Since then, The EU has taken this further with the CSRD requiring that all large enterprises trading in the EU (regardless of where they are based) disclose their emissions and those of their value chain. While Australia’s National Greenhouse Energy Reporting (NGER) system is long established (since 2007), the Albanese Government is working towards a more comprehensive set of disclosure rules. The objective is to bring the NGER in line with international best practice and to tackle the complex tracking of Scope 3 emissions.

This will aid in Australia’s goal to reduce emissions by 43% on 2005 levels by 2030 and net zero emissions by 2050, as outlined in the Climate Change Act 2022.

These trends and shifts in the landscape are not going unnoticed by investors, and they are factoring exposure to Scope 3 liabilities into risk calculations. In May 2023, AirTrunk announced that the company has linked 100% of its AU$5 billion debt funding platforms to sustainability commitments.

Challenges of managing Scope 3

There appears to be a strong case for identifying and managing Scope 3 emissions – why, therefore, is the industry slower to act than they were with that of Scope 1 and 2 and other efficiency initiatives?

The sources of Scope 1 and 2 emissions are easy to identify and well-defined, even though the challenges in dealing with them can still be considerable. Scope 1 emissions are direct. They result from a data centre’s operations, such as diesel for back-up power and natural gas, refrigerants, chemicals or fuels used as part of the construction, or the fuel used by staff to get to and from work. Scope 2 emissions are indirect, such as those produced by electricity, steam or chilled water provided through a utility.

Scope 3 is less easy to identify and define. Mark Deguara explains some of the complexities of improving the Scope 3 impact from Schneider’s perspective.

Firstly, Scope 3 brings in very strongly the need for awareness of the whole dynamic ecosystem, both upstream and downstream and this may be complex. One company can occupy different places along the stream in relation to various other organisations: one company’s scope 1 and 2 is another’s scope 3.

To take the example of Schneider itself, Deguara explains:

“A data centre perspective is fundamentally about looking at the physical building itself, so the concrete, the steel etc. and it looks at the equipment that’s being supplied via a vendor. Schneider Electric is a solution provider, both from a software perspective and very much from a hardware perspective for the data centre environment. We have therefore become a big player in a data centre’s Scope 3 requirements”.

Schneider Electric is taking a number of steps to reduce the carbon impact of its supply chain, including ‘The Zero Carbon Project’ with an objective to reduce, by 50%, the Scope 1 and 2 impacts of its top 1,000 suppliers. A further initiative looks to continue developing a circular supply chain and focussing on eliminating single use plastics, using recycled cardboard for packaging and increasing the volume of green metals and plastics used in its products by 50%.

Another source of complexity is the time scale of the impact process, particularly where the carbon is embedded:

“If you look at data centre equipment, for example, at a UPS [Uninterruptible Power System] that gets supplied and delivered to the customer. The process of manufacturing, delivery and operation uses energy, of course, but the physical box itself has embodied carbon that will remain in the facility for maybe 15 years or more. The embedded carbon of that product doesn’t just disappear once it’s in the facility, it’s there for the longevity of the system. And then the question becomes, what do you do with that product at the end of its life, if it isn’t recyclable or isn’t reusable? And this holds true for any product supporting the data centre.”

The difficulties of managing Scope 3 are accentuated by the lack of globally-established metrics. While the analogy of financial accounting is often used in relation to the process of measuring Scope 3, the value of the analogy is limited, since sustainability accounting has no industry-agreed standards or protocols. Rather, the metrics appear more subject to context and interpretation, for example, in defining the point at which an organisation needs to start setting and monitoring targets for Scope 3 reduction. Mark Deguara explains further that while standards are being applied there is no industry accepted benchmark.

“One of the difficulties for the industry is around standards for products that take the actual product and its embedded carbon emissions over its life cycle. So, that includes the manufacture of it, the transport of it, installation, removal and the disposal or recycling of it. At the moment, there’s no clear or single global or industry standard that says this is the reference point”.

Deguara also points out that the absence of such metrics makes purchasing decisions between different options less clear in a market which is becoming more conscious of Scope 3 exposure. For this reason, Schneider Electric is aligning itself with ‘PEP Ecopassport’ – an independent third-party organisation, to assess and accredit its products.

There is some concern that as data centres become more widespread and grow to meet increased demand for their services, Scope 3 can be seen as a penalty for success. Global cloud providers have needed to increase their computing workloads by considerable degrees over the past decade with only fractional increases in their energy consumption. The move towards Net Zero for Scope 1 and 2 has been accelerated through the effective deployment of offsets. The reduction in Scope 3 emissions has evidently not matched that restraint and is still very much a work in progress.

Taking Scope 3 forward

Managing Scope 3 requires identifying the key sources of emissions and reducing them through changes to operational and procurement practices.

Since there may be considerable volumes of emissions data drawn from multiple sources, there are steps that can be taken to make the process more manageable and the data more accurate. An intuitive, and structured data collection and analysis process will make it easier to identify actions to be taken based on the data.

The Scope 3 measurement process needs to factor in the nature of the data centre under study – enterprise on-prem, colocation or hyperscale. Also a critical consideration is the stage that the centre is at on their sustainability journey, whether the organisation is only just beginning to think about sustainability in relation to its data centres or whether initiatives are already in place.

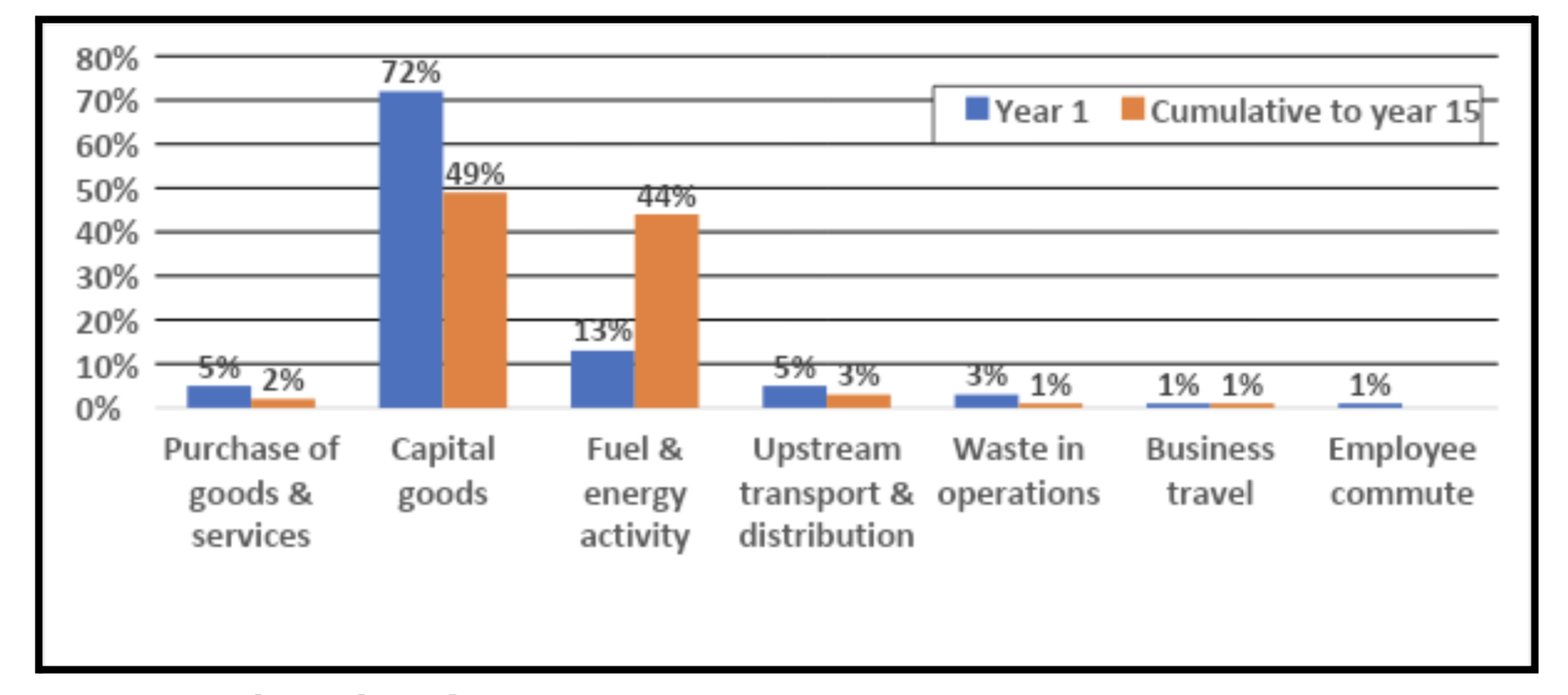

In this context it is important to identify the sources of emission and their contribution to the overall emissions profile. The chart below is taken from research conducted by Schneider Electric and it indicates that in the first year of a data centre’s life, capital goods account for almost three-quarters of the facility’s emissions and fuel/energy activity for around 13%. Cumulatively to year 15, the proportion accounted for by capital goods drops to just under half while fuel and energy activity has risen to 44%. This clearly presents the importance of Scope 3 analysis in the procurement of capital goods throughout the life of the data centre, as up to year 15 this is still the largest source of emission.

Source: Schneider Electric

Source: Schneider Electric

Schneider Electric takes their analysis of Scope 3 further in terms of source categories and metrics. These analyses can be found in the White Paper listed below.

As with other sustainability initiatives there may, in time, be legislative drivers encouraging the management of Scope 3 emissions, but for now, there are major corporate and financial drivers to doing so.

The recycling of goods, extending the life of equipment and improving planning and procurement strategies to buy what you need, and when, as well as not compromising the promises of an identity based on sustainability, all make good business sense.

Therefore, Mark Deguara stresses the urgency of looking at Scope 3:

“It [Scope 3 emissions] needs to be considered now because that embodied carbon is going to stay there. The decisions you’re making today about what you’re putting into your facility are going to still be there in 10, 15, 20 years. And if you think that Scope 3 is something you can push down the road, then the challenge there is it’s going to impact you at some point down the road because what you decide today is going to have a future impact. You can’t just move a physical box – it doesn’t work that way”.

To get closer to dealing with Scope 3 and the challenges it entails means some changes in thinking. Ultimately, Scope 3 means a commitment needs to be made to a circular economy – minimising waste, changing legacy selection criteria and a shift in the way business relationships are viewed. Rather than suppliers and customers, the view moves closer to partnerships:

“Sustainability is a journey. We as a supplier can’t solve your Scope 3 problems in isolation. It is a journey, and you need to work with your suppliers and vendors around that Scope 3 journey”.

The legacy view of the data centre operating in isolation, he believes, needs to shift to a view across the whole ecosystem and the wider requirements to manage carbon emissions:

“It’s not a data centre problem in isolation. The issue of scope 1, 2 and 3 is a wider industry issue. The challenge is not a challenge for data centres alone”.

Further Reading:

White Paper 53: Inventory for data centre scope 3 emissions : https://go.schneider-electric.com/WW_202306_SP-Global-CnSP-Web-Gating-WP53_EA-LP.html