Australia’s rapidly expanding data centre sector is becoming an increasingly significant factor in the country’s energy transition, with electricity demand from cloud and AI workloads expected to create new pressures on networks, renewable supply and grid planning, according to Fitch Ratings. The ratings agency said that while data centres create opportunities to support investment in generation and transmission infrastructure, they are also introducing additional complexity into an energy system already balancing affordability, reliability and decarbonisation targets.

According to Fitch, Australia’s business and industrial grid consumption is forecast to increase to 253TWh by 2050 from 133TWh today, with data centres supporting AI and cloud services contributing 29TWh of that increase, citing AEMO’s Draft 2026 Integrated System Plan.

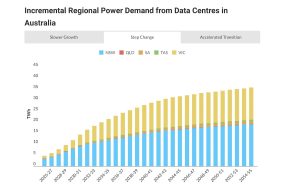

AI and hyperscale demand reshape power requirements

Fitch said traditional cloud services are likely to remain the primary source of demand growth in the near term, but AI workloads are expected to become an increasingly important driver of future capacity requirements.

“These workloads are significantly more power-intensive and require higher rack densities, advanced cooling systems and low-latency connectivity,” the company said. Fitch’s analysis, using the scenario framework from AEMO’s Draft 2026 Integrated System Plan, projects incremental electricity demand attributable specifically to data centres across three scenarios.

Under the Accelerated Transition scenario, that demand rises from around 5TWh in 2025-26 to almost 43TWh by 2054-55. Even under a slower growth scenario, incremental demand still reaches almost 20TWh over the same period.

The projections also suggest growth will continue to be concentrated heavily in Australia’s largest markets. Under the accelerated scenario, New South Wales accounts for the largest increase at around 23.6TWh by 2054-55, followed by Victoria at approximately 17.4TWh. The remaining growth is spread across Queensland, South Australia and Tasmania.

The outlook broadly mirrors current market activity, where Sydney and Melbourne continue to dominate large-scale hyperscale and AI-driven developments.

Renewable targets under pressure before data centre load

Fitch said that Australia’s energy transition is already facing headwinds that predate the data centre surge. Federal and state governments have implemented incentive schemes to encourage investment in renewable generation, storage and transmission, but the pace of deployment would need to accelerate for legislated emission-reduction and renewable-energy targets to be met. Transmission bottlenecks and permitting delays remain key challenges, and the additional load from data centres risks widening the gap further.

At the same time, Fitch noted that rising data centre demand could support new renewable and storage investment. Long-term power purchase agreements struck by large operators could improve revenue visibility for renewable and battery projects, supporting their financing and accelerating deployment — a potential credit positive for the sector.

Competition to intensify

Fitch said rising demand from large-load users such as data centres is likely to increase competition for grid access, renewable energy supply and investment capital. “Growing barriers to entry in top-tier locations, particularly in relation to power availability, is spurring new developments across secondary markets where power, water and land availability are less restricted,” the agency said.

The comments align with trends already emerging across Australia, where developers are increasingly looking beyond traditional hubs towards markets with stronger power availability and fewer infrastructure constraints.

Construction risk low, but funding structures set to evolve

Fitch said that construction risk on data centre projects remains relatively low compared with other infrastructure assets, given short build schedules and limited complexity. Pre-leasing typically occurs early in the development cycle, with sponsors often securing land but commencing construction only once a tenant is in place. In primary markets, the capacity for major developers to expand is increasingly a function of secured land, power and regulatory approvals rather than construction capability.

The agency also suggested the economics of future developments may change as projects become more closely tied to energy infrastructure requirements. “Future data centre developments may require more than investment in buildings and internal fittings,” Fitch said. “As policy settings evolve, sponsors may also need to fund transmission upgrades, firming capacity, renewable procurement and water infrastructure linked to cooling needs.”

This could increase both development costs and financing requirements, while also changing how projects are funded. Fitch expects the use of debt financing in Australia to broaden to include senior debt, asset-backed lending, project financing, green financing and private credit. The agency said larger operators with stronger liquidity, established lender relationships and demonstrated ability to secure power at scale are likely to be better positioned.

Regulatory cost recovery a key variable

For electricity utilities, the credit implications of rising data centre load will depend significantly on regulatory outcomes. Fitch said that while stronger demand may support investment in new generation, storage, transmission and distribution infrastructure, the benefit to utilities will depend on whether regulatory frameworks allow efficient and timely recovery of the costs required to accommodate large new loads. If cost recovery is delayed or unclear, higher capital expenditure could weigh on leverage and cash flow.

Energy transition increasingly tied to digital infrastructure

The report suggests that discussions around data centre growth are increasingly shifting beyond the issue of building additional renewable generation. Australia has introduced a range of policies designed to accelerate investment in renewables, batteries and transmission infrastructure, but Fitch said that transmission bottlenecks and permitting delays remain significant challenges.

The implication, which is evidenced elsewhere, is that future growth in AI and cloud infrastructure may depend less on constructing buildings and more on securing access to increasingly constrained energy resources.