As the U.S data center market scrambles to keep up with demand, the North America Data Center Trends H2 2025 report from CBRE finds that electricity has become the industry’s primary constraint over land, capital, or permitting. As a result, developers are shifting strategy towards bringing power to a planned data center site and building facilities where large, reliable power sources already exist.

Meanwhile, vacancy rates remain at historic lows, and utilities across several regions are facing long procurement timelines as a wave of greenfield proposals fills interconnection queues, leaving projects stalled even after financing and permits are secured.

“Bring Your Own Power” strategies gain momentum

To work around these constraints, developers are changing how they power their facilities. “Bring your own power,” or BYOP, is becoming a common feature in proposals submitted to utilities. Large campuses increasingly incorporate on site generation, often natural gas turbines paired with battery storage to supplement or partially replace grid supply. These hybrid power strategies allow developers to move projects forward while reducing reliance on utilities during peak load periods.

The shift has implications beyond engineering. In several regions, community sentiment is becoming a decisive factor in whether projects proceed. Loudoun County, Virginia, the largest data center market in the world illustrates the tension. By 2026, data centers there are projected to account for nearly half of local property tax revenue. At the same time, residents are raising questions about land use, noise and workforce impacts, making public engagement a critical step in the approval process.

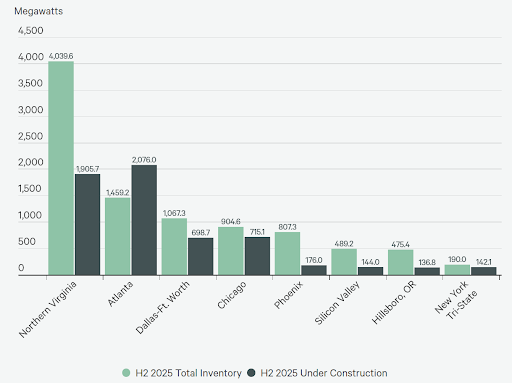

Gap between primary and secondary markets widens

Pricing reflects the imbalance in the primary markets such as Northern Virginia, Silicon Valley, Phoenix and Dallas where leasing requirements between 250 and 500 KW are expected to exceed US$ 200 per KW per month. Smaller markets still have areas of existing inventory willing to discount to attract tenants, but the spread between core and secondary locations continues to widen.

The geography of the industry is shifting as well. Southern California, the Austin, San Antonio corridor and Central Washington now collectively hold more data center inventory than the New York tristate region, marking the first time that balance in the sector has tipped since 2016. Smaller tertiary markets are beginning to compete with established hubs. Development pipelines in places like Reno, Nevada, and Abilene, Texas, could surpass those in long standing technology centers such as Hillsboro, Oregon, or Silicon Valley by 2026.

Development pipelines face regulatory and utility bottlenecks

Yet the construction pipeline itself may not grow much further in the near term. Many planned facilities remain stuck in early planning stages as developers navigate zoning approvals, environmental reviews and the increasingly complex process of securing utility capacity and new legislations. The result is a paradox as massive demand paired with a development pipeline that cannot accelerate quickly enough to meet it.

Readers will recall that new legislation is also hindering data center development, such as the Eagan City Council in Minnesota has reportedly approved a one-year moratorium on data centers and cryptocurrency operations. The council cited the need for a deeper understanding of the environmental, economic, and community impacts of these projects before allowing further development.

States compete with incentives to attract AI infrastructure

At least 36 states now offer targeted incentives designed to attract data center investment. Tax abatements, equipment exemptions and infrastructure subsidies have become standard tools as governments compete for the economic activity associated with artificial intelligence infrastructure.

Advances in long haul fiber networks and the explosive demand for AI model training have opened markets far from traditional carrier hotels in dense urban cores. A recent hyperscale deployment in West Des Moines, Iowa described by industry insiders as an “AI factory” demonstrates how high density facilities can now operate efficiently outside conventional tech corridors.

Investors target power rich regions for Gigawatt scale campuses

Investors are increasingly eyeing large, power rich sites capable of supporting gigawatt scale campuses. Parts of Ohio, Michigan, Texas and Pennsylvania have emerged as contenders, offering large tracts of land and comparatively faster access to power.

Early demand centered on massive clusters used to train AI models. Attention is shifting toward “inference” the process of running trained models in real time applications. Because inference workloads need to operate close to end users, companies are beginning to distribute smaller, high performance facilities across regional markets rather than concentrating everything in hyperscale hubs.

Conclusion

The result is an industry racing to scale while confronting the physical limits of energy, infrastructure and workforce. Demand from artificial intelligence shows little sign of slowing. The question for developers is not whether more data centers will be built but where the power, land and labour will come from to build them.