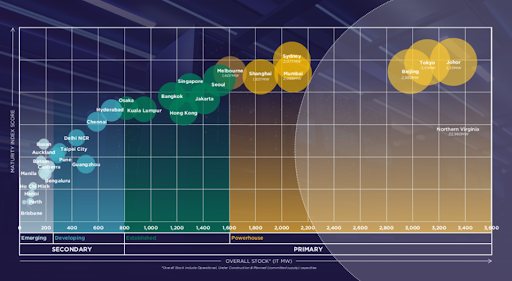

According to a recent report by Cushman & Wakefield, North East Asia’s (NEA) data center markets are strengthening their infrastructures, as the region moves from AI and cloud expansion plans to large-scale expansions across key hubs including Tokyo, Seoul, Hong Kong and Taiwan.

The report titled APAC Data Centre Update: H2 2025 | SG, finds that the NEA market has shifted decisively from AI and cloud ambition to large-scale execution, as hyperscale campuses break ground and capital concentrates on AI-optimised platforms. Although some hyperscalers moderated near-term activity, cloud providers continued launching new regions and AI-focused developments, reinforcing Asia Pacific’s position as a primary destination for digital infrastructure investment.

Operational supply across NEA approached record levels, supported by hyperscale pre-leasing, AI-driven compute requirements and sustained capital inflows. Moreover, development pipelines continued to expand, with capacity under construction and in planning rising steadily alongside tightening vacancy rates in core markets. While power constraints and land scarcity remain structural challenges in several metros, cloud service providers and AI operators continued launching new regions and high-density deployments, reinforcing NEA’s role as a critical center digital infrastructure.

Here’s a closer look at the report’s findings pertaining to key NEA digital infrastructure markets.

Tokyo: Reinforces its lead as AI fuels Asia-Pacific data center expansion

Tokyo has reinforced its standing as Japan’s leading data center market as it remains one of only four Asia-Pacific hubs with over 1GW of operational capacity. Total pipeline supply rose 8 percent year-on-year (YoY) to 1.93 GW, even as developers grappled with land scarcity and tightening power availability.

Leasing accelerated in the second half of 2025, driving vacancy down to 5.6 percent from 9 percent in 2024. Demand has been led by hyperscale cloud providers and AI-related deployments, particularly high-density model training. In response, operators are ramping up liquid cooling adoption and next-generation rack designs, while tenants increasingly pre-commit to capacity amid supply constraints.

Tokyo now accounts for 77 percent of Japan’s operational stock and 57 percent of its development pipeline, underscoring the market’s concentration. To ease grid pressure, the government in January 2026 launched the Watt-Bit Collaboration Initiative, with a pilot involving the University of Tokyo, TEPCO Power Grid and Fujitsu to redistribute compute workloads to regions with surplus power.

Separately, Japan is stepping up investment in next-generation supercomputing. RIKEN, Fujitsu and NVIDIA are co-developing FugakuNEXT, a hybrid AI–HPC system expected to deliver more than five times the hardware performance of the current Fugaku machine and up to 100 times application-level gains. The Ministry of Economy, Trade and Industry has also allocated JPY 72.5 billion (US$ 470 million) across five national AI supercomputing programmes, with Sakura Internet receiving the largest funding share.

Hong Kong: Muted activity but strong pipeline

Hong Kong recorded muted data center development activity in the second half of 2025, with colocation vacancy holding at 19 percent. The wider economy exceeded expectations as Growth Domestic Product (GDP) expanded 3.5 percent, marking a third consecutive year of growth and bolstering investor sentiment.

Authorities pushed forward with the Northern Metropolis strategy, launching a major data center land tender at Sandy Ridge that is expected to deliver 250,000 sqm of new capacity. At the same time, Grand Ming Group explored the sale of its iTech Tower portfolio, attracting preliminary interest from global investors including Bain Capital and Actis, although no deal has been finalized.

Looking ahead, the pipeline signals a more active expansion phase. Sixteen projects totalling roughly 670MW are planned or under construction, including 161MW currently being built, pointing to a stronger development cycle over the next three to five years.

Seoul: Decentralisation and global capital drive expansion

Seoul posted 16 percent YoY growth in operational data center capacity to 601 MW, while its development pipeline expanded 43 percent to approximately 921 MW, underscoring sustained capital inflows and investor demand.

The market is undergoing a structural decentralisation with 30 percent live capacity is now located outside Seoul’s traditional core clusters, as power limitations and elevated land costs drive operators toward peripheral districts and alternative cities with greater scalability.

Global technology firms are accelerating commitments. Amazon Web Services has pledged an additional US$ 5 billion for AI-focused infrastructure, adding to a prior US$ 4 billion programme that included an AI data center in Ulsan developed with SK Group. Meanwhile, OpenAI is advancing plans for a Stargate AI data center in partnership with Samsung Electronics and SK Hynix, intensifying competition to scale next-generation AI capacity.

Taiwan: Consolidates fundamentals despite modest growth

Taiwan recorded modest data center capacity growth of 3 per YoY to 110MW in the second half of 2025, while its development pipeline expanded to 195MW. Market fundamentals tightened notably, with colocation vacancy falling from 16 percent to 5.6 percent, signalling stronger demand conditions.

Artificial intelligence–driven investment is gathering pace as GMI Cloud is planning a US$ 500 million AI infrastructure project featuring around 7,000 NVIDIA GB300 GPUs and 16MW of power capacity, with commercial launch targeted for March 2026. Separately, Microsoft confirmed plans for a new Azure cloud region in Taiwan scheduled to become operational in 2026 to improve latency performance and data residency support.

The regional market is shifting toward AI-optimised, high-density compute infrastructure. Tokyo remains the largest-scale hub, while Seoul continues to attract capital inflows. Hong Kong is positioning for renewed supply expansion, and Taiwan is tightening fundamentals as cloud adoption and AI workload deployment accelerate across the region.

Asia-Pacific’s data center sector is moving into a new expansion cycle, underpinned by accelerating artificial intelligence adoption and sustained hyperscale cloud investment. Market dynamics are diverging across the region, with supply concentration, infrastructure constraints and capital inflows shaping development patterns. Operators are increasingly prioritising high-density, AI-optimised computing environments as demand shifts toward large-scale model training and advanced workload deployment.