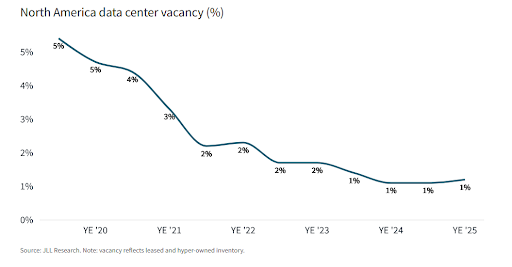

North America’s data center market is operating at near full capacity, with vacancy holding at a mere 1 percent for a second straight year, according to the latest market report from JLL. The firm’s year-end 2025 analysis shows 39 GW of active capacity across the region, split between leased space and facilities owned by hyperscale operators.

Limited supply is pushing up pricing as rents rose 9 percent in 2025, in line with a five-year compound annual growth rate of 10 percent with large requirements above 1 MW increasing by 13 percent. In a press release, 64 percent of the 35 GW under construction is located outside traditional hubs such as Northern Virginia, Dallas-Fort Worth and Silicon Valley.

Texas alone accounts for 6.5 GW underway, putting it on track to surpass Virginia as the world’s largest data center market by 2030. Tennessee, Wisconsin and Ohio are also attracting large projects, aided by power availability, land and business incentives with more than 10 projects of at least 1 GW are currently being built.

Andy Cvengros, Executive Managing Director and Co-Lead of U.S. Data Center Markets, JLL, said, “Record-low vacancy sustained over two consecutive years provides compelling evidence against bubble concerns. This structural change is driven by hyperscale and AI demand and development headwinds that will likely keep vacancy near zero for the next several years.”

Andrew Batson, Global Head of Data Center Research, JLL said, “With rents up 60 percent since 2020, landlords are capturing significant rent spreads on renewals while tenants continue to experience pronounced sticker shock on new leases. Most leases being executed today include annual escalations of 3 percent or more, with little to no concessions.”

Between 2025 and 2030, continued development is anticipated across both colocation facilities and owner-operated (self-built) data centers, largely to accommodate AI-driven compute intensity. Geographically, market activity is increasingly shifting from Tier 2 to Tier 3 metropolitan areas, where greater power availability and scalability enable the development of gigawatt-scale campuses. In April 2025, the U.S. Department of Energy (DOE) identified 16 potential sites deemed suitable for AI data center campus deployment, further reinforcing the sector’s expansion trajectory.

Hyperscale cloud providers are driving capital spending, with the top five planning a combined US$ 710 billion in 2026 expenditures. AI firms including OpenAI and Anthropic were tied to roughly 10 GW of project announcements in 2025. Grid interconnection timelines, often four years or longer, are forcing tenants to secure power and capacity well in advance, accelerating the shift into emerging markets.

According to Arizton Intelligence, the U.S. data center market reached an investment value of US$ 208.38 billion in 2024, and is projected to grow to US$ 308.83 billion by 2030, reflecting a compound annual growth rate (CAGR) of 6.78 percent over the forecast horizon. Expansion is being propelled primarily by accelerating demand for artificial intelligence (AI) workloads, prompting substantial capacity buildouts by hyperscale cloud operators, internet service providers, and AI-focused enterprises.