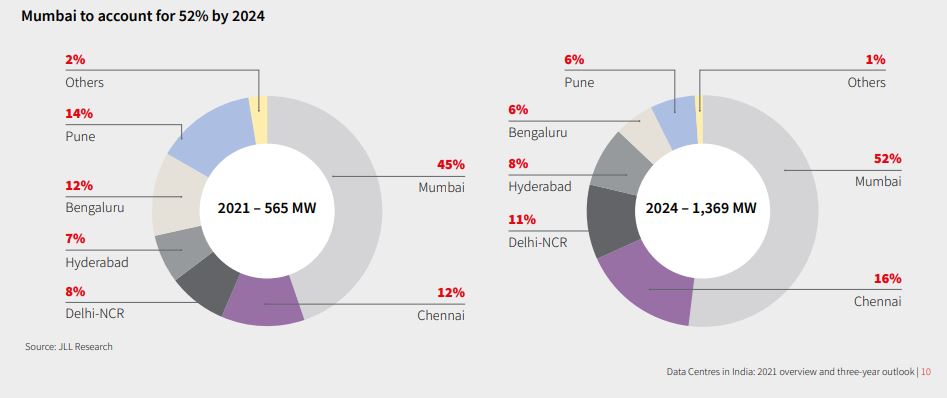

Capacity expansion by existing and new players in the data centre industry is expected to result in an additional capacity of 804 MW during 2022-2024, translating to 34 per cent CAGR for the period, according to JLL’s report India’s data centre report card 2021.

A notable feature of this supply growth has been that a large share has been pre-committed by hyperscale and is expected to become operational in the next three years, JLL said. Mumbai and Chennai to lead in capacity expansion Mumbai and Chennai are expected to witness higher growth owing to their infrastructure advantages.

As a result, both cities will account for 68 per cent of the total capacity in 2024. The addition of a new cable landing that would connect these cities, going forward, would also lead to higher bandwidth.

Landlocked locations like NCR-Delhi would also see growth in capacity addition due to government-led digital initiatives and data demand. Proactive state policies, meanwhile, are creating Hyderabad into an emerging location for hyperscale cloud players, the report added.

Real Estate demand

The Indian data centre industry is expected to add 804 MW capacity from 2022-to 2024. This would mean the creation of 9.7 million sq ft of real estate space for this new capacity across India’s leading cities. Since data centre construction is driven by the design specifications of each operator, the nature of this capacity addition would differ across data centre hubs in the country. However, data centre hubs in India are most competitive in terms of land, construction, mechanical, electrical and plumbing costs.

“Owing to its high share of capacity addition, Mumbai is expected to create demand for 6.18 million sq ft, going forward. The comparatively high land cost of the city vis-à-vis other data centre hubs will lead to a higher outlay of USD 3.3 billion for setting up data centres in the city. As Chennai has similar advantages, it would follow with 2.03 million sq ft of real estate space addition at an investment of USD 1 billion,” said Rachit Mohan, Head, data centre Advisory, India, JLL.

The report further explained that the strong demand growth has been matched by a supply addition of 119 MW during the year, registering a growth of 23 per cent over 2020. Mumbai, Pune, and Chennai together accounted for 83 per cent of the total supply during 2021.

Data centre operators have been following a land banking strategy to provide scalable and seamless options for hyperscale cloud players. In the Mumbai region, the Navi-Mumbai suburb has emerged as a preferred location due to its high-capacity power station, developed territorial cable connectivity, and availability of land at a lower cost than the mainland. Hyperscale cloud players have been exploring various availability zones to ensure seamless operations. The expected growth in demand is likely to lead to strong capacity addition during 2022-2024.

The year that was

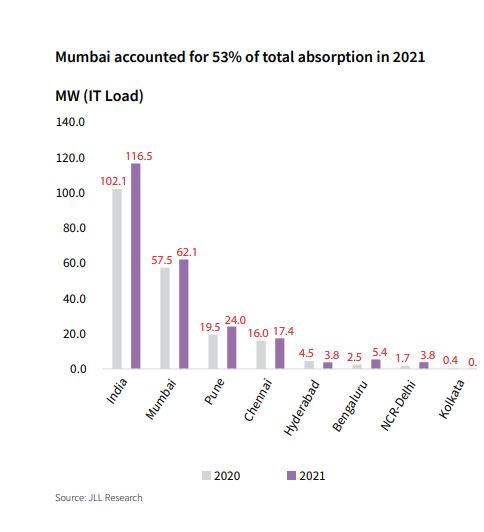

The demand momentum for the data centres that picked up during 2020 has gained pace, with an estimated absorption of 116 MW during 2021, a 14 per cent Year-on-Year (Y-o-Y) Hyperscale cloud players accounted for 69 per cent of this absorption, as pre-committed capacities were delivered during the year. Hyperscale cloud allows businesses to expand their IT infrastructure based on its demand. Mumbai accounted for 53 per cent of the total absorption as the preferred location of leading cloud players.

The sector’s three basic conditions of power supply, connectivity and customer base are amply provided by the city, making it the default location of data centre operators. Pune accounted for 21 per cent of the total absorption, followed by Chennai at 15 per cent. The need to diversify across regions, as well as the emergence of strategic locations and favourable regulatory policies, is leading to an expansion trend across India’s key data centre hubs.

“Demand picked up in the second half of 2021 in India’s key markets, including Mumbai. In fact, the total absorption in the second half of the year increased by 49 per cent over the first half. In Mumbai alone, demand increased by a strong 71 per cent in the second half of 2021, reaching 62 MW for the year.

This demand was led primarily by cloud players and BFSI firms expanding their footprints. The data centre market is standing at the threshold of high growth as hyper-scale cloud players aggressively expand their capacities for a slice of the growth pie. The expected boom in data consumption with the convergence of various technologies has also led to various players building up capacities,” said Dr. Samantak Das, Chief Economist and Head of Research & REIS at JLL India.

He further added that this high growth is currently being matched by ambitious growth plans of colocation data centre operators, leading to a capacity addition of 119 MW during the year. The untapped potential from other sectors like agriculture, logistics, finance and automotive also promises a high growth trajectory for data usage in the years ahead.

A joint study titled ‘Data Centres: The building blocks of the digital revolution in India,’ by Nxtra by Airtel and JLL India showed that the convergence of data protection, strong demand from cloud players, migration from captive to cloud, industry-friendly regulations, government’s digital initiatives, and investments will spearhead the ongoing growth of the data centre industry in India.

According to Nxtra by Airtel and JLL analysis, much of the industry growth will centre around Mumbai and Chennai due to their business and infrastructure advantages, strategic location, and cable landing stations that are well-positioned to support and enable the growth of data centres across India.