Energy is no longer just another expense line for data centres. It’s one of the largest operating costs on the P&L, a board-level issue, a sustainability priority, and increasingly, a competitiveness issue.

If a data centre already has redundancy, backup generation, and sophisticated control systems, why should that infrastructure sit idle as insurance? Can this cost line be repurposed to provide revenue and facilitate more renewable electricity on the Australian grid?

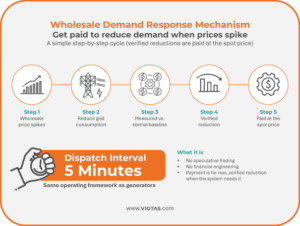

Australia’s Wholesale Demand Response Mechanism (WDRM), introduced into the National Electricity Market in 2021, creates a practical opportunity for large energy users to monetise flexibility that already exists inside their operations. In simple terms, when wholesale electricity prices spike, a large user can reduce grid consumption and be paid the prevailing spot price for that reduction.

Dispatch occurs in five-minute intervals; the same framework used for generators. Performance is measured against a baseline of normal consumption. If load is reduced during a dispatch interval, that verified reduction is settled at the wholesale price. There’s no speculative trading or financial engineering. It’s simply being rewarded for lowering demand when the system needs it.

Most businesses would struggle to participate meaningfully in a mechanism like this. Data centres are different.

Data centres are engineered for resilience. Redundancy is built in. On-site generation is standard. UPS systems sit in the background, and increasingly batteries are part of the architecture. Add real-time monitoring and controls, and the capability to respond is already there.

Participation can involve temporarily switching to on-site generation, using battery storage, optimising cooling loads, or adjusting non-time-critical processes. Crucially, it can be structured and controlled. Operators define thresholds, determine how conservative participation should be, and can choose not to dispatch if conditions aren’t right.

From a CFO lens, this is an asset productivity story. Backup infrastructure is capital intensive and traditionally justified purely on reliability grounds. WDRM introduces the ability to extract incremental value from those same assets without changing the reliability equation. For larger facilities, particularly 10MW and above, even selective participation during extreme price events can meaningfully offset energy costs and improve returns.

Operationally, the first concern is always reliability. That concern is valid and manageable.

Dispatch is short and frequent (five-minute intervals), and participation is typically engineered conservatively. Clear load hierarchies are established in advance. Controls are automated. Governance is defined. The load offered into WDRM is not exposed to spot prices during that interval, keeping the commercial structure clean. This isn’t about adding risk. It’s about using flexibility deliberately.

A broader market shift is also underway. As renewable penetration increases, price volatility tends to increase. At the same time, reforms are progressing toward a more “two-sided” market where demand participates alongside generation.

Neil Morris, former Amazon Web Services Ireland Country Lead and European Operations Director, and Senior Advisor to VIOTAS, notes: “The energy mix supplying the grid is becoming more complex, with a growing share of less predictable renewable generation replacing traditional thermal sources. At the same time, data centres are an increasing proportion of overall demand. This creates a clear responsibility for operators to act as good grid citizens, designing and building grid-integrated data centres that actively support system stability rather than simply consuming power.”

In that environment, flexible load becomes strategically valuable.

Data centres, by design, are among the most controllable large loads in the system. That’s not a weakness, it’s leverage. Increasingly, operators are asking a smarter question: if we already have the capability, why wouldn’t we use it more intelligently?

WDRM is one pathway. Frequency Control Ancillary Services (FCAS) and emerging capacity mechanisms are others. The common theme is clear: energy infrastructure is no longer just passive protection sitting in the background. It’s programmable, revenue-capable, and becoming part of competitive positioning.

Over time, the differentiator won’t only be uptime. It will be how intelligently the megawatts behind that uptime are managed.

Author: Lisa Balk, Director of Sales, VIOTAS Australia